Are my investment choices appropriate for me as I approach retirement?

In the years approaching retirement you should be identifying what benefits you are likely to take from your pension plan at retirement.

Along with the decision what benefits to take, you need to know if you are invested in appropriate funds.

- Check if you are invested in an investment strategy which automatically invests you in lower risk funds which match your likely retirement benefits the closer you get to retirement.

View longer answer

Irish Life Corporate Business offers the Personal Lifestyle Strategy (PLS) which automatically switches you into lower risk funds which match your likely retirement benefits. To find out more about PLS and how the fund switches work in your years before retirement watch this video.

- If you are not invested in a strategy already, you should find out if there is a strategy available and how it will work for you.

- Check to see if you are invested in appropriate funds to suit the benefits you are aiming for in retirement and your attitude to risk.

- Review your documents and talk to your financial advisor.

This is the big question. After all those years of contributing to your retirement fund, finally the time comes to choose your retirement benefits.

If you retire at the normal retirement age (usually age 65, depending on your plan rules), the pension fund you have built up over the years may provide the following options.

- Cash lump sum and/or

- Annuity and/or

- Approved Retirement Fund (ARF)

For more information on each of these options, see below.

What are my

options at

retirement?

options at

retirement?

What are

my cash lump

sum options?

my cash lump

sum options?

You have some options as to how you will take your cash lump sum. This depends on what type of pension savings arrangement you have. Also, some of your cash lump some may be taken tax free at retirement, up to certain limits.

View longer answer

Cash Lump Sum

You have some options as to how you will take your cash lump sum. This depends on what ype of pension savings arrangement you have. Please read through these options below to see what is appropriate for you.

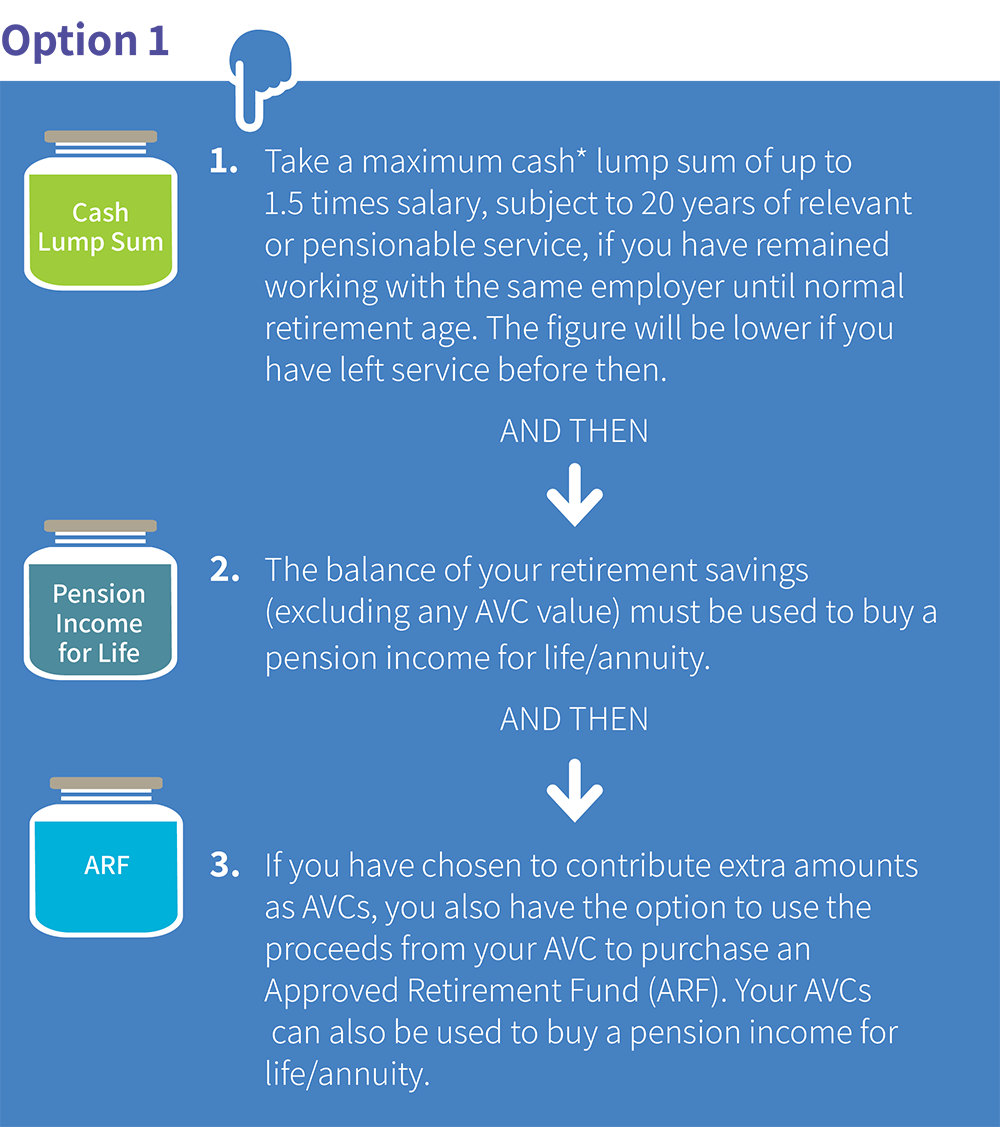

The following Option 1 applies to Defined Benefits and Defined Contribution Plans:

You can find explanations of ARFs in other sections of our Frequently Asked Questions.

*Scroll down on this page for the likely tax treatment of lump sums.

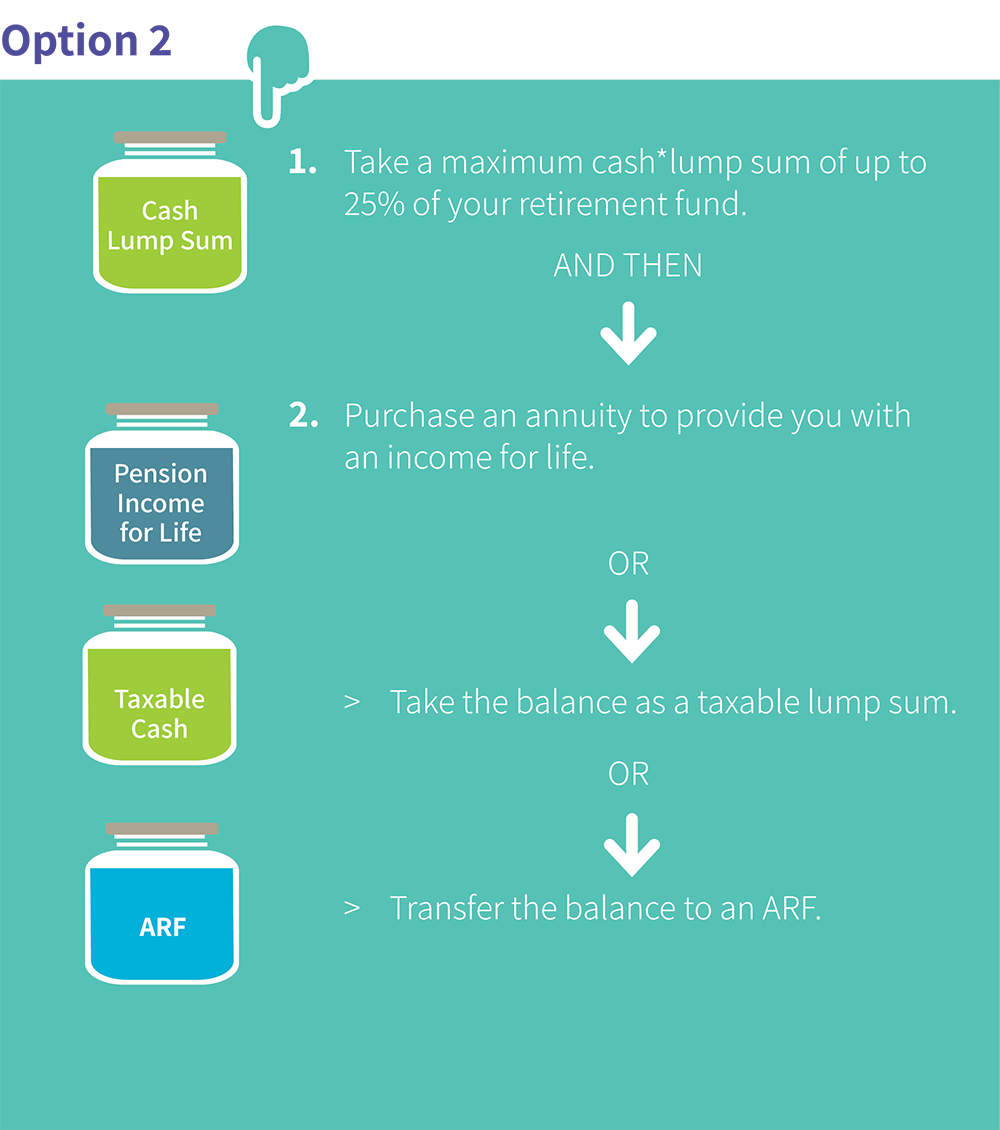

The following Option 2 applies to Defined Contribution Plans and PRSAs (Personal Retirement Savings Accounts)

*Scroll down on this page for the likely tax treatment of lump sums.

If you have a Personal Retirement Bond (PRB) your cash lump sum option depends on the type of pension savings arrangement you are transferring from. If you are transferring from a Defined Contribution arrangement the date your transfer occurred will affect the options available. If your PRB was set up before 7 February 2011 then you may only avail of option 1. If your PRB was set up after the 7 February 2011 then you may be able to avail of either option 1 or option 2.

If you are transferring from a DB arrangement, then option 1 will be available to you.

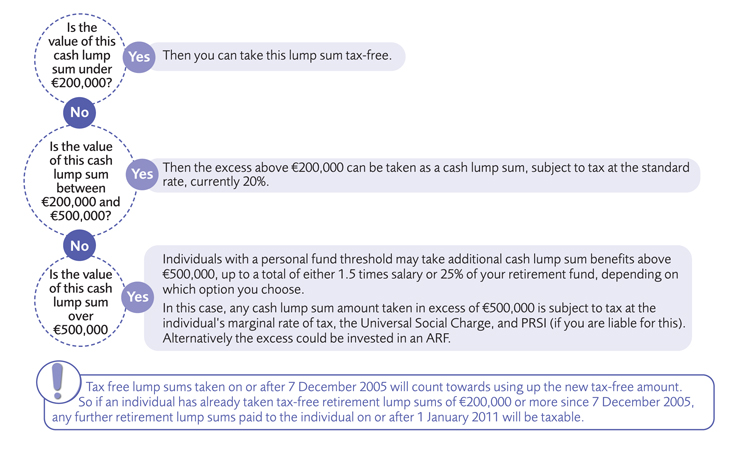

Likely tax treatment

Some of your cash lump some may be taken tax free at retirement, up to certain limits. The likely tax outcomes we outline here for your cash lump sum are suitable for the following arrangements:

• Defined Contribution (DC)

• Personal Retirement Bond (PRB)

• Personal Retirement Savings Account (PRSA)

• Defined Benefit (DB) arrangement

* The Standard Fund Threshold allowable for tax relief purposes will reduce from €2.3m to €2.0m in January 2014 (as proposed by the Finance Bill 2014) This maximum amount includes any pension benefits already taken together with pension benefits yet to be taken. Any fund in excess of this amount will be liable to a once off income tax charge at the top rate of tax (currently 41%) when it is drawn down on retirement. A personal fund threshold might be higher if you have agreed this with Revenue in the past.

Figures are correct as at May 2022.

Members of Defined Contribution schemes should ensure that their retirement options take into account all relevant factors in order to maximise the Cash Lump Sum allowable. The 4 key factors are:

- Salary

- Total Service

- Retained Benefits i.e. do you have pension benefits with another pension provider/employer or have you transferred benefits from a previous pension arrangement into this one

- Can you make a last minute Single Premium Payment

View longer answer

How can I maximise my cash lump sum at retirement?

Members of Defined Contribution schemes should ensure that their retirement options take into account all relevant factors in order to maximise the Cash Lump Sum allowable. The 4 key factors are:

Salary

Revenue rules permit a number of options in relation to the salary on which the Cash Lump Sum is based.

- The salary* in the year in which you retire

- The highest salary* in the last 5 years

- The average of the highest 3 consecutive years salaries* in the previous 10 years

*This can be the Gross salary as per the P60 plus pension contributions for that year, or the rate of salary at a particular point during that year.

You should note that the average of certain non-salary payments e.g. BIK, overtime may be used to increase the salary for Revenue limit purposes.

Alternatively, a person can take 25% of the value of the fund as a Cash Lump Sum.

Please note that the maximum overall amount of Cash Lump Sum that an individual can draw down tax free from pension arrangements over his/her lifetime is €200,000.

Total Service

- Ensure the date of joining service and the date service ceases are accurate

- It is also important to ensure that any Transfer Values paid into the current pension arrangement are taken into account and that the Cash Lump Sum is not solely based on the service with the current employer

Retained Benefits

- If you have pension benefits with more than one pension provider/employer it is very important that you make each of them aware of the other pension benefits to ensure that the Cash Lump Sum is calculated within Revenue limits

Can you make a last minute Single Premium Payment

- You may be eligible to make a last minute Single Premium payment to the pension scheme before you retire in order to maximise your Cash Lump Sum. Please discuss this with your financial adviser before making any payment to ensure that this is the best course of action for you. Also see our information on last minute AVCs, watch this video which might help and read through the AVC webpage.

What if I receive more

than one pension?

than one pension?

For tax purposes, if you are in receipt of more than one pension you should contact your Local Inspector of Taxed to advise them of the pensions you are receiving. They will then be able to send Tax Credit and Universal Social Charge Certificates to your pension providers to allow them tax your pensions at the correct rates.

When you retire, some or all of your pension fund may be used to purchase a lifetime retirement pension which is also called an annuity . The purpose of this pension annuity is to provide an income for the rest of your life, no matter how long you live. An annuity suits those who have a low appetite for risk and demand certainty of income in retirement. Irish Life offers both standard and enhanced annuities. An enhanced annuity provides an income which is tailored to your own lifestyle and health circumstances.

Related Links

Annuities

What is an

annuity?

annuity?

What happens to my

pension/annuity

when I die?

pension/annuity

when I die?

When you retire a pension (or annuity) is purchased to provide you with an income in retirement which will be paid for as long as you live.

This pension may have features such as a minimum guaranteed payment period or a dependants pension which becomes payable if you predecease the dependant for whom the dependants pension was purchased. We have provided a brief description of what happens when you die based on the type of annuity that was purchased when you retired.

View longer answer

- If a single life pension was purchased for you and there was a guaranteed payment period which ended prior to your death, your pension simply ends when you die.

- If a joint life pension was purchased for you and you predecease the dependant the joint life pension was purchased for the relevant pension amount will then be paid to your dependant for the rest of their life when you die.

- If a single life investment protection pension was purchased and you have received gross pension payments totalling less than the purchase price paid for your pension, the balance will be paid to your estate when you die. You will need to discuss the taxation implications of this with your financial adviser as the tax treatment of any balance remaining differs depending on who receives the amount remaining after you die.

If you are trying to figure out how best to arrange your pension based on what will happen to your pension when you die, you should talk to your financial adviser.

An Approved Retirement Fund (ARF) is a personal retirement fund where you can keep your money invested after retirement as a lump sum. With an ARF you managed and control your retirement fund and can invest it in a wide range of different investment funds. You can withdraw from it regularly to give yourself an income, on which you pay income tax, the Universal Social Charge (USC) and PRSI (if you are liable for this). Any money left in fund after your death will pass to your estate. More details in relation to this are set out in the related link below.

Related Links

Approved Retirement Fund

What is

an ARF?

an ARF?

When can I claim my

company pension?

company pension?

You can take retirement benefits from your Defined Contribution (DC) company pension when you stop working for your employer provided you are either over age 50 or are retiring because of ill health. Trustee consent is normally required. If you take your benefits early the value you get could be a lot less than if you had claimed your benefits at age 65.

However, if you are still working and have reached normal retirement age in the employment to which the company DC pension plan relates you can claim your company pension and continue to work, assuming your employer agrees.

Additional Voluntary Contributions (AVCs) are extra contributions you can make to your pension scheme in order to increase your benefits when you retire. Depending on your circumstances AVCs can be very tax efficient for you.

Related Links

Additional Voluntary Contributions

What are Additional

Voluntary Contributions?

Voluntary Contributions?

What if I have more

than one pension policy

to use for providing

retirement benefits?

than one pension policy

to use for providing

retirement benefits?

You might want to consider whether you wish to consolidate your policies into one arrangement or keep them as separate policies. Contact your financial adviser who will help you with this.

Yes, all income in Ireland is subject to taxation. This applies to your pension and any other income you receive in retirement too.

Your income from your pension will be taxed under the PAYE system of taxation.

View longer answer

Will my

pension be

taxed?

pension be

taxed?

All income in Ireland is subject to taxation. This applies to your pension and any other income you receive in retirement too. You need to make sure your pension is taxed correctly and that you are benefiting from any tax credits you may have.

To ensure your Irish Life pension is taxed correctly:

- Step 1. When your pension payments start, contact your local inspector of taxes to advise that you are now in receipt of retirement income. Details of your local tax office can be found on the following page www.revenue.ie

- Step 2. Give them your PPS Number.

- Step 3. Ask them to allocate all or a portion of any available tax credits you have to Irish Life.

- Step 4. Confirm Irish Life’s Tax Reference Number. You should choose the appropriate Tax Reference Number for your retirement income from the following list:

- Annuity: For a regular annuity payment, tax credits should be allocated to Irish Life (Pension Payments) under tax reference number 0087900D.

- ARF and Vested PRSA: For ARF or vested PRSA withdrawals and other taxable payments, tax credits should be allocated to Irish Life (ARF Payments) under tax reference number 4820009C

The local inspector of taxes will tell you the correct rate of income tax that you should pay on your pension. Confirmation of your tax liability is then sent to Irish Life in the form of a Tax Credit & Universal Social Charge Certificate.

Until Irish Life receives this Certificate from the local inspector of taxes, advising of the tax we should deduct from your pension income, you will be taxed on an Emergency Tax Basis.

So it is in your interest to get this certificate to us as soon as possible.

How can I look after my

spouse/registered civil

partner or dependants if I

predecease them when I

retire?

spouse/registered civil

partner or dependants if I

predecease them when I

retire?

You can decide to use the money that you have built up in your pension fund to provide a pension income (also called annuity) for:

- just you or

- a pension income which will be paid first to you and then will become payable to your spouse/registered civil partner or dependants if you predecease them.

View longer answer

You can decide to use the money that you have built up in your pension fund to provide a pension income (also called annuity ) for you only, or a pension income which will be paid first to you and then will become payable to your spouse/registered civil partner or dependants if you predecease them.

Making these provision means that you will receive a lower monthly pension than if you only make provision for yourself. The reduction in your pension is related to the level of benefits chosen for your financial dependants and to a lesser extent the age gap between you and your financial dependants.

If you invest in an Approved Retirement Fund (ARF) then on your death the ARF will form part of your estate. The taxation treatment of any fund passed to your estate will depend on who inherits the fund.

| Inherited by | Income Tax | Capital Aquisition Tax |

| Surviving spouse | No tax due on the transfer to an ARF in the spouse's name | No |

| Children (under 21) | No tax due | Yes, taxable inheritance |

| Children 21 and over | Yes (30%) | No |

| Others (including surviving spouse/civil partner if benefit paid out as a lump sum) | Yes, at deceased's tax rate at the time of death (either 20% or 41%) | Yes, taxable inheritance. Spouse and civil partner are exempt. |

Remember that any death benefits (usually called death in service benefits) which you were covered for before retirement under your occupational pension scheme will automatically cease when you leave service. They may also cease when you reach your normal pension date even if you continue working past your normal pension date.

It may be possible for your death in service benefits to remain in force if you continue working after your normal pension date subject to satisfactory medical evidence.

Yes you can. Even if Irish Life Corporate Business looked after your pension savings up until now, you are not obliged to then purchase your pension, also called an annuity, with us. You can choose to buy your pension/annuity from another provider - this is called the open market option. You should compare different pension/annuity offers from the various providers and along with your financial advisers, choose the one that most suits you.

Can I shop around

when it comes to

buying my pension?

when it comes to

buying my pension?

Can I continue

to work after taking

my benefits?

to work after taking

my benefits?

From a pension perspective, if you’ve taken your benefits at normal retirement age, yes. But this is really a question for your employer.

View longer answer

If you employer does allow you to continue working past your normal retirement age you have a number of options in relation to your pension:

- Take all your pension benefits at normal retirement age.

- Take your maximum cash lump sum and leave any remaining amount in the scheme until you retire.

- Do not take any pension benefits and continue to make pension contributions to scheme if you so wish. The pension benefits can then be taken in full when you retire.

Note –

- Pension benefits must be taken no later than age 70 regardless of whether your employer allows you to continue to work beyond that age.

- If your pension scheme allows you to take benefits after age 50 and before your normal retirement age you cannot make any further contributions or continue in the employment to which the scheme related.

You can take your pension benefits from a previous employment and continue to work once you satisfy the following criteria:

- You are over age 50.

- You no longer work for the employer that the pension benefits relate to.

- The trustees of the pension scheme allow you to take the pension benefits (if you are taking them before your normal retirement age).

There are specialised courses to help you plan for your retirement. One of the organisations that run these courses is the Retirement Planning Council of Ireland.

The aim of these courses is to help you understand what to expect in your retirement and how best to prepare for the exciting time ahead.

Related Links

Retirement Planning Council of Ireland

Are there any

retirement preparation

courses available?

retirement preparation

courses available?

When can I

get the State

Pension?

get the State

Pension?

From 1 January 2014 the State Pension (Contributory) is payable from age 66.

Legislation was passed to keep the State Pension age at 66: The Social Welfare Act 2020 was signed on 22 December 2020 and this deleted the relevant provision (Section 7 of the Social Welfare and Pensions Act 2011) which would have increased the State Pension age to 67 from 01/01/2021 and to 68 from 01/01/2028.

There is now no provisions in legislation to trigger a future increase to the State Pension age. New legislation will need to be passed if the State Pension age is to rise. In order to consider this further the Government has established a Commission on Pensions, as set out in the programme for government. The Commission will examine sustainability and eligibility issues in respect of State Pension arrangements and will outline options for Government to address issues such as State Pension qualifying age, PRSI contribution rates, total contributions and eligibility requirements.

Find out more about the different types of State Pensions available.

View longer answer

Related Links

State Benefits

The State Pension (Contributory)

The age at which the State Pension becomes available will rise over the next few years.

State Pension (Contributory) payable

From age 66 from 1 January 2014

The State Contributory Pension is not means tested. It is based on the average number of PRSI contributions you have made each year. As at October 2013 the maximum rate of the State Contributory Pension is €230.30 per week and the current minimum rate is €92 per week. There are additional increases for qualified adult dependants but these are means tested. The State Pension (Contributory) is subject to income tax but you do not pay the Universal Social Charge on this pension. You should notify your local inspector of taxes when you start to receive this pension.

When should I apply to receive the State Contributory Pension?

You should apply to the Department of Social Protection for your State Pension at least 3 months before you reach age 66. However if you paid social insurance contributions in more than one country, you should apply 6 months before your 66th birthday. Full details regarding the State Pension are available in the Welfare website.

Contributory Widow's, Widower's and Surviving Civil Partner's Pension

To qualify for this pension you must of course, be a widow, widower or surviving civil partner and you must not be cohabiting with another person. You do not pay the Universal Social Charge (USC) on this pension. There is lots more information available on this pension in the Welfare website

The State Pension (Non-Contributory)

If you do not qualify for the State Contributory Pension, an alternative Non-Contributory State Pension, which is means tested, is available. You may qualify for the State Pension (Non-Contributory) if:

• You are aged 66 or over

• You do not qualify for an State Pension (Contributory)

• You pass a means test

• You meet the habitual residence condition

For more information regarding the State Non-Contributory pension visit the Welfare website.

Other State benefits

In addition to State pensions, there are a number of additional benefits payable to retired or older people. These include, free travel, a household package that includes help with electricity, gas and your TV licence. There are a number of conditions that need to be met in order to receive these benefits and you will need to check these conditions when you retire.

In addition to a pension there are other State Benefits available:

- Household Benefits

- Free Travel

- Medical Benefits

View longer answer

Are there any

other State benefits

available when

I retire?

other State benefits

available when

I retire?

Household benefits

If you satisfy a number of conditions you may also qualify for the Household Benefits Package. There are two allowances in the Household Benefits Package:

1. The Electricity Allowance or Natural Gas Allowance or Cash Electricity Allowance or Cash Gas Allowance

2. The Free Television Licence

Full details regarding the household benefits are available in the Welfare website.

Free travel

The Free Travel Scheme operated by the Department of Social Protection allows people who are aged 66 or over and who are permanently residing in the State, to travel free of charge on most CIE public transport services, LUAS, as well as on the public transport services of a large number of private operators in various parts of the country. Certain incapacitated people under age 66 are also entitled to free travel.

Full details regarding free travel are available in the Welfare website.

Medical benefits

A medical card may be obtained by anybody at age 70 on a means tested basis. The HSE updated the Medical Card/GP Visit Card National Assessment Guidelines for people aged 70 years and over (pdf) in April 2013.

This information is only an outline of some State benefits available to you. For more information please see some additional resources available:

www.welfare.ie

www.citizensinformation.ie

Who should I contact for

further information?

further information?

If you want more information in relation to your retirement planning you should contact your broker or financial adviser. Or if you have a pension with Irish Life Corporate Business you can also contact us at code@irishlife.ie or call 01 704 1845.